Semidefinite programming

From Wikipedia, the free encyclopedia

Semidefinite programming (SDP) is a subfield of convex optimization concerned with the optimization of a linear objective function over the intersection of the cone of positive semidefinite matrices with an affine space, i.e., a spectrahedron.Semidefinite programming is a relatively new field of optimization which is of growing interest for several reasons. Many practical problems in operations research and combinatorial optimization can be modeled or approximated as semidefinite programming problems. In automatic control theory, SDP's are used in the context of linear matrix inequalities. SDPs are in fact a special case of cone programming and can be efficiently solved by interior point methods. All linear programs can be expressed as SDPs, and via hierarchies of SDPs the solutions of polynomial optimization problems can be approximated. Finally, semidefinite programming has been used in the optimization of complex systems.

Contents |

Motivation and definition

Initial motivation

A linear programming problem is one in which we wish to maximize or minimize a linear objective function of real variables over a polyhedron. In semidefinite programming, we instead use real-valued vectors and are allowed to take the dot product of vectors. Specifically, a general semidefinite programming problem can be defined as any mathematical programming problem of the form![\begin{array}{rl}

{\displaystyle \min_{x^1, \ldots, x^n \in \mathbb{R}^n}} & {\displaystyle \sum_{i,j \in [n]} c_{i,j} (x^i \cdot x^j)} \\

\text{subject to} & {\displaystyle \sum_{i,j \in [n]} a_{i,j,k} (x^i \cdot x^j) \leq b_k \qquad \forall k}. \\

\end{array}](http://upload.wikimedia.org/wikipedia/en/math/f/8/8/f88255c018dce0154f44961e90618d9b.png)

Equivalent formulations

An matrix

matrix  is said to be positive semidefinite if it is the gramian matrix of some vectors (ie. if there exist vectors

is said to be positive semidefinite if it is the gramian matrix of some vectors (ie. if there exist vectors  such that

such that  for all

for all  ). If this is the case, we denote this as

). If this is the case, we denote this as  . Note that there are several other equivalent definitions of being positive semidefinite.

. Note that there are several other equivalent definitions of being positive semidefinite.Denote by

the space of all real symmetric matrices. The space is equipped with the inner product (where

the space of all real symmetric matrices. The space is equipped with the inner product (where  denotes the trace)

denotes the trace)

We can rewrite the mathematical program given in the previous section equivalently as

in

in  is given by

is given by  from the previous section and

from the previous section and  is an matrix having th entry

is an matrix having th entry  from the previous section.

from the previous section.Note that if we add slack variables appropriately, this SDP can be converted to one of the form

as a diagonal entry (

as a diagonal entry ( for some

for some  ). To ensure that

). To ensure that  , constraints

, constraints  can be added for all

can be added for all  . As another example, note that for any positive semidefinite matrix , there exists a set of vectors

. As another example, note that for any positive semidefinite matrix , there exists a set of vectors  such that the ,

such that the ,  entry of is

entry of is  the scalar product of

the scalar product of  and

and  .

Therefore, SDPs are often formulated in terms of linear expressions on

scalar products of vectors. Given the solution to the SDP in the

standard form, the vectors can be recovered in

.

Therefore, SDPs are often formulated in terms of linear expressions on

scalar products of vectors. Given the solution to the SDP in the

standard form, the vectors can be recovered in  time (e.g., by using an incomplete Cholesky decomposition of X).

time (e.g., by using an incomplete Cholesky decomposition of X).Duality theory

Definitions

Analogously to linear programming, given a general SDP of the form

and

and  ,

,  means

means  .

.Weak duality

The weak duality theorem states that the value of the primal SDP is at least the value of the dual SDP. Therefore, any feasible solution to the dual SDP lower-bounds the primal SDP value, and conversely, any feasible solution to the primal SDP upper-bounds the dual SDP value. This is because

Strong duality

Under a condition known as Slater's condition, the value of the primal and dual SDPs are equal. This is known as strong duality. Unlike for linear programs, however, not every SDP satisfies strong duality; in general, the value of the dual SDP may lie strictly below the value of the primal.(i) Suppose the primal problem (P-SDP) is bounded below and strictly feasible (i.e., there exists

such that

such that  ,

,  ). Then there is an optimal solution

). Then there is an optimal solution  to (D-SDP) and

to (D-SDP) and

for some

for some  ). Then there is an optimal solution

). Then there is an optimal solution  to (P-SDP) and the equality from (i) holds.

to (P-SDP) and the equality from (i) holds.Examples

Example 1

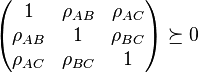

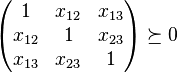

Consider three random variables ,

,  , and . By definition, their correlation coefficients

, and . By definition, their correlation coefficients  are valid if and only if

are valid if and only if

and

and  . The problem of determining the smallest and largest values that

. The problem of determining the smallest and largest values that  can take is given by:

can take is given by:- minimize/maximize

- subject to

to obtain the answer. This can be formulated by an SDP. We handle the

inequality constraints by augmenting the variable matrix and introducing

slack variables, for example

to obtain the answer. This can be formulated by an SDP. We handle the

inequality constraints by augmenting the variable matrix and introducing

slack variables, for example

Solving this SDP gives the minimum and maximum values of

as

as  and

and  respectively.

respectively.Example 2

Consider the problem- minimize

- subject to

whenever .

whenever .Introducing an auxiliary variable

the problem can be reformulated:

the problem can be reformulated:- minimize

- subject to

.

.The first restriction can be written as

is the square matrix with values in the diagonal equal to the elements of the vector

is the square matrix with values in the diagonal equal to the elements of the vector  .

.The second restriction can be written as

- det

![\underbrace{\left[\begin{array}{cc}t&c^Tx\\c^Tx&d^Tx\end{array}\right]}_{D}\geq 0](http://upload.wikimedia.org/wikipedia/en/math/4/7/1/4716c3a1c00adcf62801a21e76330fdb.png)

.

.The semidefinite program associated with this problem is

- minimize

- subject to

![\left[\begin{array}{ccc}\textbf{diag}(Ax+b)&0&0\\0&t&c^Tx\\0&c^Tx&d^Tx\end{array}\right] \succeq 0](http://upload.wikimedia.org/wikipedia/en/math/a/7/3/a73fe310dadd0470b5e627217fa60e1a.png)

Example 3 (Goemans-Williamson MAX CUT approximation algorithm)

Semidefinite programs are important tools for developing approximation algorithms for NP-hard maximization problems. The first approximation algorithm based on an SDP is due to Goemans and Williamson (JACM, 1995). They studied the MAX CUT problem: Given a graph G = (V, E), output a partition of the vertices V so as to maximize the number of edges crossing from one side to the other. This problem can be expressed as an integer quadratic program:- Maximize

such that each

such that each  .

.

- Relax the integer quadratic program into an SDP.

- Solve the SDP (to within an arbitrarily small additive error

).

). - Round the SDP solution to obtain an approximate solution to the original integer quadratic program.

such that

such that  , where the maximization is over vectors instead of integer scalars.

, where the maximization is over vectors instead of integer scalars.

;

since the vectors are not required to be collinear, the value of this

relaxed program can only be higher than the value of the original

quadratic integer program. Finally, a rounding procedure is needed to

obtain a partition. Goemans and Williamson simply choose a uniformly

random hyperplane through the origin and divide the vertices according

to which side of the hyperplane the corresponding vectors lie.

Straightforward analysis shows that this procedure achieves an expected approximation ratio

(performance guarantee) of 0.87856 - ε. (The expected value of the cut

is the sum over edges of the probability that the edge is cut, which is

proportional to the angle

;

since the vectors are not required to be collinear, the value of this

relaxed program can only be higher than the value of the original

quadratic integer program. Finally, a rounding procedure is needed to

obtain a partition. Goemans and Williamson simply choose a uniformly

random hyperplane through the origin and divide the vertices according

to which side of the hyperplane the corresponding vectors lie.

Straightforward analysis shows that this procedure achieves an expected approximation ratio

(performance guarantee) of 0.87856 - ε. (The expected value of the cut

is the sum over edges of the probability that the edge is cut, which is

proportional to the angle  between the vectors at the endpoints of the edge over

between the vectors at the endpoints of the edge over  . Comparing this probability to

. Comparing this probability to  , in expectation the ratio is always at least 0.87856.) Assuming the Unique Games Conjecture, it can be shown that this approximation ratio is essentially optimal.

, in expectation the ratio is always at least 0.87856.) Assuming the Unique Games Conjecture, it can be shown that this approximation ratio is essentially optimal.Since the original paper of Goemans and Williamson, SDPs have been applied to develop numerous approximation algorithms. Recently, Prasad Raghavendra has developed a general framework for constraint satisfaction problems based on the Unique Games Conjecture.[1]

Algorithms

There are several types of algorithms for solving SDPs. These algorithms output the value of the SDP up to an additive error in time that is polynomial in the program description size and  .

.Interior point methods

Most codes are based on interior point methods (CSDP, SeDuMi, SDPT3, DSDP, SDPA). Robust and efficient for general linear SDP problems. Restricted by the fact that the algorithms are second-order methods and need to store and factorize a large (and often dense) matrix.Bundle method

The code ConicBundle formulates the SDP problem as a nonsmooth optimization problem and solves it by the Spectral Bundle method of nonsmooth optimization. This approach is very efficient for a special class of linear SDP problems.Other

Algorithms based on augmented Lagrangian method (PENSDP) are similar in behavior to the interior point methods and can be specialized to some very large scale problems. Other algorithms use low-rank information and reformulation of the SDP as a nonlinear programming problem (SPDLR).Software

The following codes are available for SDP:SDPA, CSDP, SDPT3, SeDuMi, DSDP, PENSDP, SDPLR, ConicBundle

SeDuMi runs on MATLAB and uses the Self-Dual method for solving general convex optimization problems.

No comments:

Post a Comment

Thank you